Railway operators throughout Asia are progressively broadening their commercial pursuits beyond the traditional realm of passenger fares, as metro and commuter rail networks continue to expand in both scale and complexity. While fare revenue constitutes the primary source of income for most systems, rising operational costs, regulated fare structures, and the substantial financial requirements of infrastructure expansion have necessitated that operators investigate alternative revenue streams.

Non-fare revenue, such as property development, retail operations at stations, advertising, and commercial leasing, has emerged as a crucial element for the financial sustainability of railway systems. In numerous Asian contexts, particularly those possessing robust property development rights, commercial income now constitutes a significant proportion of total revenue. This diversification not only facilitates reinvestment in infrastructure but also enables the maintenance of affordable fare structures.

This transformation signifies a broader shift in the role of railways within urban economies. Leading railway operators are evolving to function not only as transport providers but also as integrated developers and managers of urban commercial ecosystems constructed around railway infrastructure.

Financial Pressure on Fare-Dependent Rail Systems

Urban rail systems generally operate under regulated fare regimes that aim to keep public transport accessible and affordable for all users. While this policy effectively supports broader community mobility and inclusion, it simultaneously limits the potential for revenue growth for transport operators. This limitation becomes increasingly critical as railway systems grapple with escalating operating costs driven by factors such as energy consumption, routine maintenance, asset renewal, and network expansion.

In large metropolitan areas, rail networks require ongoing, significant investment across multiple areas, including modern signalling systems, timely rolling stock replacement, and crucial infrastructure upgrades to meet the demands of a growing population. The challenge is that fare revenue alone seldom covers the full lifecycle costs of these essential improvements, resulting in financial strain on operators.

In response to this financial pressure, many rail operators have begun seeking alternative revenue streams to supplement income through commercial activities beyond passenger fares. International research on metro system financing has shown that operators that diversify their revenue structures tend to be more financially resilient. This diversity not only lessens the reliance on government subsidies but also enhances the overall sustainability of the transport services provided.

In Asia, several progressive railway operators have successfully transformed non-fare income into a significant component of their financial performance. Strategic land development rights and innovative commercial strategies have typically supported this success. By optimizing available land around stations and integrating a range of commercial ventures, from retail spaces to real estate developments, these operators have established robust revenue streams that complement fare collections, ultimately bolstering their financial health and operational capabilities.

Non-Fare Revenue Performance Among Leading Asian Rail Operators

The scale of non-fare revenue generated by railway operators varies widely, influenced by factors such as regulatory frameworks, property ownership structures, and the strategic approaches to commercial development that each operator employs. For instance, some operators may leverage extensive real estate holdings to generate additional income through leasing, while others might diversify revenue through retail partnerships, advertising spaces, or service enhancements. To illustrate these differences, the following comparison provides an overview of the estimated contributions of non-fare income for selected railway operators across Asia, highlighting the impact of their unique business models and market conditions on their overall revenue generation strategies.

Railway Operator | Country / Region | Core Network Type | Key Non-Fare Revenue Sources | Estimated Non-Fare Revenue Share |

MTR Corporation | Hong Kong | Urban metro and suburban rail | Property development, retail leasing, and advertising | ~55–60% |

JR East (East Japan Railway Company) | Japan | Urban rail and Shinkansen | Station retail, real estate, and hotels | ~35–40% |

Tokyo Metro | Japan | Urban metro | Station retail, advertising, and commercial leasing | ~20–25% |

SMRT Corporation | Singapore | Metro, LRT, bus | Retail leasing, advertising, and commercial property | ~20–30% |

Seoul Metro | South Korea | Urban metro | Advertising, station retail, leasing | ~15–20% |

Shenzhen Metro | China | Urban metro | Property development, TOD, retail leasing | ~40–50% |

Sources: MTR Corporation Annual Report 2023; East Japan Railway Company Integrated Report 2024; Tokyo Metro Annual Report 2023; SMRT Annual Report 2023; Shenzhen Metro Group disclosures; World Bank urban rail studies.

The comparison reveals a distinct trend: operators with robust access to property development rights consistently achieve markedly higher non-fare income than those that primarily rely on advertising and retail leasing for revenue. The ability to develop properties offers a substantial financial advantage, enabling these operators to create diverse revenue streams beyond traditional fare collection. In contrast, operators with restricted access to property development opportunities may find their income potential limited, relying heavily on static, often less lucrative avenues such as advertising and retail leasing to sustain their operations. This disparity underscores the importance of strategic property development in enhancing the overall financial performance of transit systems.

Property Development and Land Value Capture

Property development has increasingly become a dominant non-fare revenue mechanism within the Asian railway sector, effectively harnessing the rise in land value driven by enhanced accessibility from new rail infrastructure. This strategic approach not only supports the financial sustainability of rail systems but also stimulates urban development around transit lines.

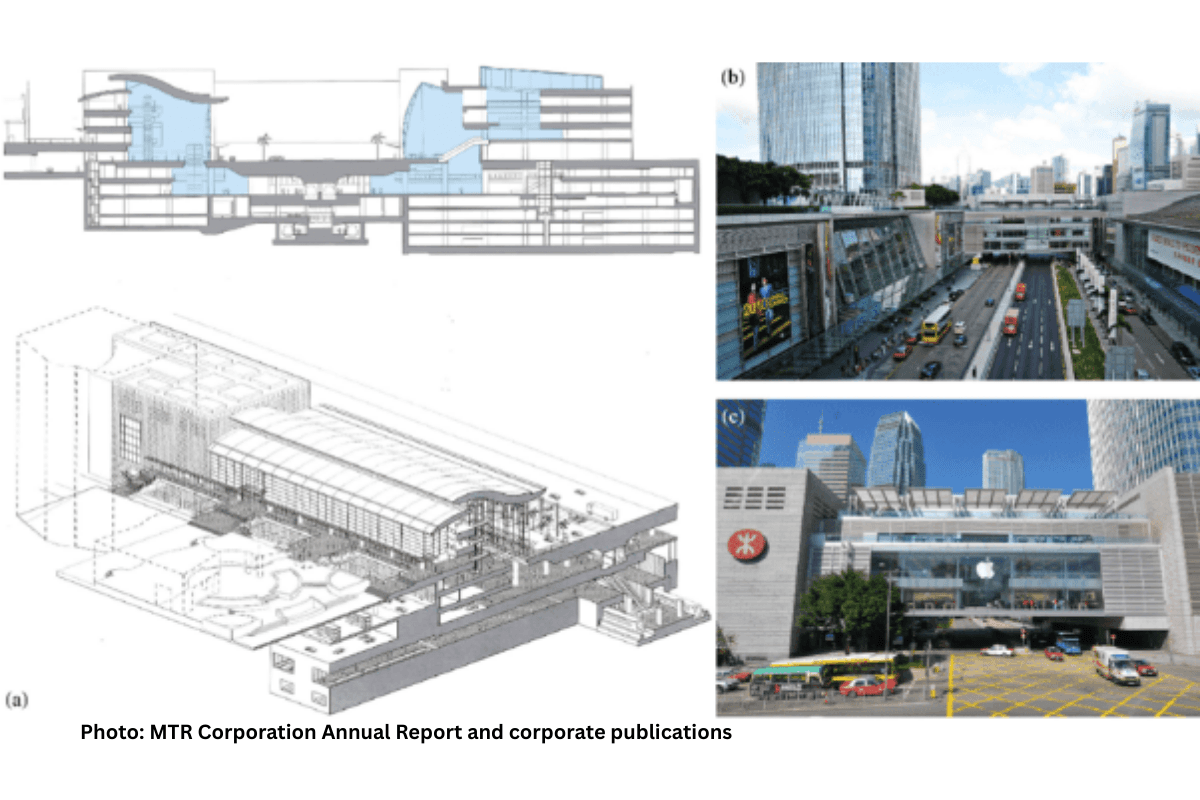

A hallmark example of this strategy is the Rail-plus-Property (R+P) model pioneered in Hong Kong. This framework allows the railway operator to secure development rights for the land surrounding future stations. In this model, the operator collaborates with private developers to create a diverse array of residential, commercial, and mixed-use projects that are seamlessly integrated with the rail network. This integration is designed not only to meet the growing demand for housing and business space but also to facilitate easier access for commuters.

The financial benefits of the R+P model are substantial. Revenue streams are generated through several avenues, including land premiums paid by developers for the right to build near transit stations, profits from development projects, and ongoing income from long-term property management. The MTR Corporation Annual Report for 2023 highlighted that the company achieved HK$4.7 billion in property rental and management revenue. Additionally, earnings from property development activities, including residential and commercial projects integrated with the metro system, have contributed significantly to the corporation's overall financial health.

This innovative model not only facilitates railway expansion but also leverages the real estate value generated by the transport infrastructure itself. By linking real estate development directly to transit initiatives, the R+P model creates a sustainable financial ecosystem in which investments in public transport are partially offset by the increased land value and economic activity that arise from improved accessibility.

In recent years, similar transit-oriented development models have gained traction in several metro systems across mainland China, including Shenzhen, Guangzhou, and Hangzhou. These cities have embraced integrating property development with new station construction, promoting a holistic approach to urban growth that reflects the successful elements of Hong Kong's R+P strategy. This convergence of transportation and urban planning illustrates a growing recognition of the importance of accessible and interconnected city environments in fostering economic activity and enhancing quality of life.

Station Retail and Commercial Ecosystems

Another major source of non-fare revenue is the commercialisation of station environments. High passenger throughput creates strong retail demand, allowing operators to transform stations into commercial hubs.

Japanese railway operators have been particularly successful in developing station-based retail ecosystems. East Japan Railway Company has implemented the "Ekinaka" concept, which integrates retail outlets within the ticketed areas of major stations. These developments include supermarkets, convenience stores, restaurants, and specialised retail services located directly within commuter circulation areas.

JR East's diversified business structure illustrates the scale of these activities. According to the company's Integrated Report 2024, non-transport businesses, including retail, real estate, and hospitality, represent a substantial component of overall revenue, supported by large station-based commercial developments in the Tokyo metropolitan region.

Major railway stations such as Tokyo, Shinjuku, and Shinagawa function not only as transport hubs but also as major retail destinations, attracting large numbers of daily visitors.

Advertising and Media Networks

Railway networks have evolved into significant advertising platforms, capitalizing on the high concentration of passengers at both stations and on trains. These environments offer unique opportunities for brands to reach diverse audiences. Advertising revenue is generated through a mix of channels, including digital displays strategically placed in high-traffic areas, eye-catching platform billboards, interior media systems on trains, and exterior branding on train cars.

The rapid digitalization of advertising infrastructure has further enhanced the commercial potential of these assets. Digital displays enable tailoring advertising campaigns to specific times of day, accommodating varying passenger flows, and targeting distinct demographic segments, allowing for a more personalized advertising experience. This adaptability makes it easier for advertisers to engage potential customers effectively.

As a result, advertising revenue has emerged as an essential supplementary income stream for railway operators. For instance, MTR Corporation reported an impressive advertising revenue of approximately HK$981 million in 2023. This revenue resurgence coincides with the recovery of passenger volumes and an increase in tourism activity following the pandemic's disruptions.

While advertising revenue typically accounts for a smaller share of total income than more lucrative ventures like property development, it plays a critical role in providing stable, recurring income that fluctuates with passenger traffic levels. The integration of advertising within the railway ecosystem not only enhances revenue but also enriches the travel experience by offering passengers relevant and engaging content.

Emerging Commercial Opportunities

Beyond the conventional scope of retail and property management, railway operators are proactively exploring a range of commercial opportunities that align with the rapidly evolving urban mobility landscape. As cities become increasingly interconnected, the importance of integrating different modes of transport is more critical than ever.

One of the pivotal developments in this space is the implementation of digital ticketing systems and mobility applications. These platforms not only streamline ticket purchasing for passengers but also generate extensive datasets that provide insights into passenger movement patterns. By analysing this data, operators can enhance targeted marketing strategies, improve mobility analytics, and offer integrated digital commerce services that cater to the dynamic needs of urban commuters. Notably, several leading railway operators in Japan and China are embracing this trend, incorporating sophisticated retail and digital payment platforms within their transport applications to create a more seamless travel experience.

Another promising avenue for growth is integrating e-commerce and logistics services into railway stations. This initiative includes installing parcel lockers, designated e-commerce pickup points, and establishing small distribution hubs in station complexes. By monetizing available space in and around stations, operators not only generate additional revenue streams but also improve the efficiency of urban logistics networks. This integration facilitates a smooth transfer of goods and services, enhancing the convenience for customers who increasingly prioritize efficiency in their shopping and travel experiences.

These innovative developments underscore the evolving role of rail infrastructure as a crucial component of digital urban mobility platforms, positioning railway operators as key players in the broader urban transport landscape. As they continue to adapt and diversify their offerings, railway systems are becoming central to the infrastructure that supports not only mobility but also the economic vitality and convenience of urban environments.

Opportunities for Southeast Asian Rail Systems

While the concept of non-fare revenue strategies has been effectively implemented across various rail systems in Asia, many Southeast Asian rail networks are in the early stages of adopting similar commercial models. Cities such as Singapore, Bangkok, Kuala Lumpur, Jakarta, Manila, and Ho Chi Minh City are actively expanding their metro and commuter rail networks to accommodate growing urban populations and enhance public transport accessibility.

As these transit systems expand, they offer significant opportunities to integrate commercial development with transport infrastructure. Transit-oriented development (TOD) around new metro stations is a particularly promising avenue. For instance, projects like the Klang Valley MRT network in Malaysia and the ongoing expansion of Bangkok's mass transit system are situated within rapidly evolving urban corridors, where rising land values create a lucrative backdrop for development.

If these initiatives are underpinned by sound planning policies and effective development frameworks, station-area development could yield substantial and sustainable long-term revenue streams for rail operators. Additional opportunities are emerging across various domains, such as station retail expansion to enhance the customer experience and increase foot traffic; the establishment of digital advertising networks that leverage dynamic displays to target commuters effectively; and the integration of mobility services that facilitate seamless connections across different modes of transport.

Partnerships focused on e-commerce logistics could revolutionize last-mile delivery, capitalizing on the strategic locations of stations to streamline operations. Collectively, these strategies not only promise to bolster the financial viability of rail systems but also enhance urban environments by fostering vibrant, multi-functional spaces that serve local communities.

Outlook

The expansion of non-fare revenue strategies marks a significant transformation in the railway sector, particularly in Asia's rapidly urbanizing landscape. Leading railway operators in the region have pioneered innovative approaches by leveraging their transport infrastructure as integrated platforms for urban development, seamlessly combining elements of property management, retail operations, and diverse commercial ecosystems.

This integrated approach allows railway companies not only to enhance passenger convenience but also to generate substantial revenue streams beyond traditional ticket sales. For cities across Asia experiencing rapid urban growth, these models offer a promising pathway to improve the financial sustainability of rail infrastructure. By aligning railway development with broader urban planning objectives, these operators can foster transit-oriented growth that enhances connectivity, reduces congestion, and promotes sustainable city living.

As metro networks continue to expand throughout the region, the skill with which railway operators can capture and harness the economic value generated in the proximity of their infrastructure will become increasingly critical. It includes creating mixed-use developments that attract both businesses and residents, ultimately enhancing ridership while securing funding for future infrastructure investments. The outcome of this strategy could redefine the economic landscape of urban areas and ensure the long-term viability and resilience of railway systems amid ongoing urbanization challenges.